品牌和营销人员为了接触到最合适的消费者,已经不得不忍受史无前例的媒体碎片化,再向他们抛出一个全球大流行病,无异于往篝火上泼汽油。

从 3 月 11 日世卫组织宣布 COVID-19 确实是一种流行病开始,任何投资回报率的愿望都已烟消云散,并引发了一场令人肃然起敬的创意内容大拍卖。

For instance, ad inventory that was purpose-built and slated to be associated with the upcoming Olympic games, for travel and tourism purposes, or simply felt tone deaf in the wake of a fast-moving, unknown virus that prompted strict social distancing measures globally, was halted and marketers pulled back. In Italy, for instance, advertisements for a train service featuring people hugging were reported as late as March 8. Following COVID-19, marketing strategies as well as creatives needed to be looked at in a whole new light.

This during a time when unprecedented levels of video viewing were increasing significantly. In mid to late March, total use of television in the U.S., including the use of digital enablers, such as smart TVs, internet-connected devices and gaming consoles, was up 18% from early March. During that same time (March 13 to 31), daily app usage increased significantly as COVID-19 spread across the U.S. compared with the first two-and-a half months of this year (Jan. 1 to March 12). This pattern followed suit across many other countries, from Italy to South Korea. The irony to marketers was that while viewers were certainly tuning in, many were and still are ostensibly “shut ins,” venturing out very little to shop, dine and socialize. The discretionary spending that went with these habits slowed down.

但是,对消费者保持沉默始终是营销人员的一种冒险行为,即使对于需要做出艰难预算决策的品牌来说也是如此。

Consider this: Advertising cuts could mean an extended recovery period for the media market. Brands that go totally dark for the rest of 2020 could be facing revenue declines of up to 11% in 2021. When you take into account that it takes up to three to five years of solid and consistent brand building effort to recover from extended “dark periods” of media, marketers who maintain brand equity by adjusting their creatives—even if that means simply adding COVID-related brand awareness messages to existing campaigns—are poised to be better positioned following any recovery, immediate or prolonged.

Among some of the top advertising categories in the U.S., not only did the amount of creative units leading up to COVID (Jan. 27-March 8) see a decline following the pandemic status (March 9-April 19), from 15.3 million to 13.3 million respectively, but so too did the share of time these categories advertised. For instance, the amount of advertising for travel was down 60%, retail declined by 21% and telecommunication ads saw a 17% drop in units. This negation in units for these categories actually gave other categories, such as automotive and financial services, a larger share of the advertising time unit-wise thus allowing companies associated with these categories a larger voice. And both the beer and wine as well as the pharmaceutical categories actually increased the amount of ads that were running following COVID.

广告市场的萎缩并不只发生在美国;全球各国的广告支出也出现了下降,这取决于各种因素,包括各国对危机的反应、民众的受影响程度以及对各自经济的影响。例如,西班牙是欧洲受影响最严重的国家之一,3 月份的广告支出比前一个月(2020 年 2 月)下降了 29%。与此相反,澳大利亚的广告支出却比上月下降了 6%,因为该国没有出现病毒的社区传播。

营销人员也认为,亟需提供以 COVID 为主题的创意,以此来表示支持,提供能够帮助消费者的商品和服务,如路边取货和非接触式送货上门,或参与某种形式的慈善活动。对许多品牌来说,这样做既能保持品牌知名度,与消费者保持联系,又不会被视为利用危机本身。

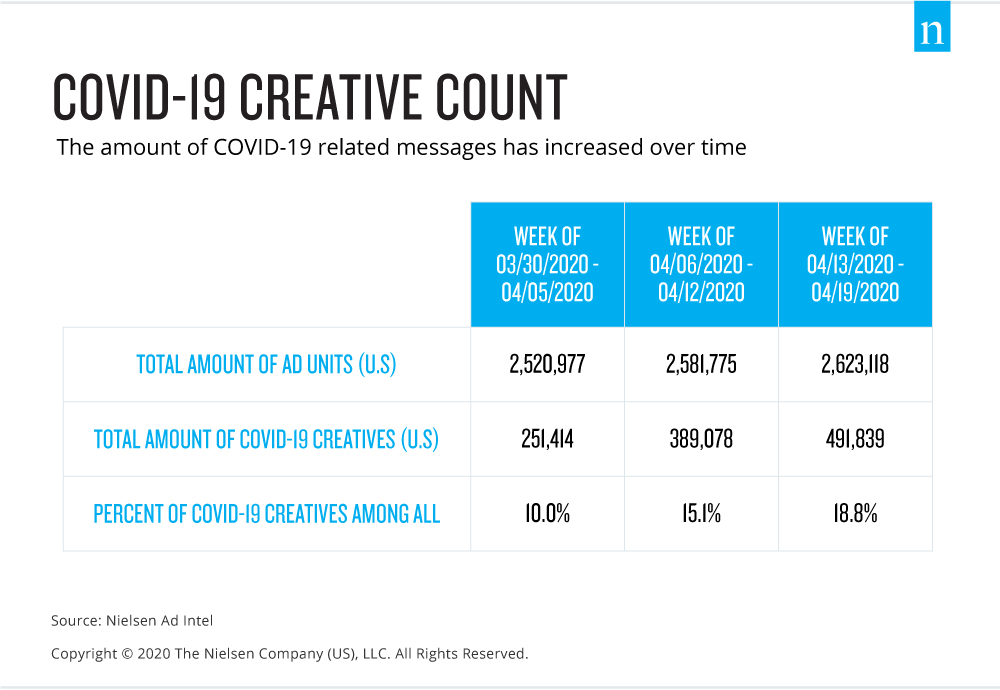

And companies did roll out an increasing amount of ads with COVID-related messages. Nielsen found that from the end of March through the middle of April alone, COVID-themed ads nearly doubled in just a few weeks alone. COVID creative units in the national and local markets jumped from 251,000 units during the week of March 30 to 492,000 units the week of April 13—a 96% increase that signals that brands understood going silent entirely was not an option for long-term health.

Consumers themselves were actually open to trying new brands that they saw as helping people during this time. A survey conducted by Nielsen and Wizer, a consumer insights platform backed by Nielsen, found that 72% of respondents cite a company’s efforts in helping people affected by COVID-19 as a reason they’d consider their brand of consumer packaged goods (CPG). What’s more is that 84% of respondents agreed that companies offering support as consumers comply with COVID restrictions are setting themselves apart from companies that do not.

But with a potential for a second wave of crisis in the fall or winter later this year in the U.S., dependent on states reopening and different emerging scenarios, these COVID-related messages are not simply ways to connect with consumers, but also a core indicator on not just the health of the media market, but also an aggregated look at how that market, and specifically marketers, think of the health of the actual consumers themselves. Declines in COVID-19 themes could act as a barometer for how ready brands think the market is for getting back to focusing on ROI and their traditional core messages. And getting back to business would be that crucial elixir that can help marketers as well as media owners revive any media stagnation.