최고의 소비자에게 도달하기 위해 이미 엄청난 미디어 파편화를 감내해야 하는 브랜드와 마케터에게 전 세계적인 팬데믹을 던지는 것은 모닥불에 휘발유를 던지는 것과 같습니다.

3월 11일 세계보건기구가 코로나19를 팬데믹으로 선언한 순간부터 ROI에 대한 열망은 사라졌고, 크리에이티브 콘텐츠의 유서 깊은 불매 운동으로 이어졌습니다.

For instance, ad inventory that was purpose-built and slated to be associated with the upcoming Olympic games, for travel and tourism purposes, or simply felt tone deaf in the wake of a fast-moving, unknown virus that prompted strict social distancing measures globally, was halted and marketers pulled back. In Italy, for instance, advertisements for a train service featuring people hugging were reported as late as March 8. Following COVID-19, marketing strategies as well as creatives needed to be looked at in a whole new light.

This during a time when unprecedented levels of video viewing were increasing significantly. In mid to late March, total use of television in the U.S., including the use of digital enablers, such as smart TVs, internet-connected devices and gaming consoles, was up 18% from early March. During that same time (March 13 to 31), daily app usage increased significantly as COVID-19 spread across the U.S. compared with the first two-and-a half months of this year (Jan. 1 to March 12). This pattern followed suit across many other countries, from Italy to South Korea. The irony to marketers was that while viewers were certainly tuning in, many were and still are ostensibly “shut ins,” venturing out very little to shop, dine and socialize. The discretionary spending that went with these habits slowed down.

그러나 소비자에 대해 침묵하는 것은 마케터에게 항상 위험한 도박이며, 예산 결정이 어려운 브랜드도 마찬가지입니다.

Consider this: Advertising cuts could mean an extended recovery period for the media market. Brands that go totally dark for the rest of 2020 could be facing revenue declines of up to 11% in 2021. When you take into account that it takes up to three to five years of solid and consistent brand building effort to recover from extended “dark periods” of media, marketers who maintain brand equity by adjusting their creatives—even if that means simply adding COVID-related brand awareness messages to existing campaigns—are poised to be better positioned following any recovery, immediate or prolonged.

Among some of the top advertising categories in the U.S., not only did the amount of creative units leading up to COVID (Jan. 27-March 8) see a decline following the pandemic status (March 9-April 19), from 15.3 million to 13.3 million respectively, but so too did the share of time these categories advertised. For instance, the amount of advertising for travel was down 60%, retail declined by 21% and telecommunication ads saw a 17% drop in units. This negation in units for these categories actually gave other categories, such as automotive and financial services, a larger share of the advertising time unit-wise thus allowing companies associated with these categories a larger voice. And both the beer and wine as well as the pharmaceutical categories actually increased the amount of ads that were running following COVID.

이러한 광고 시장의 위축은 미국에만 국한된 것이 아니라 전 세계 국가에서도 위기에 대한 각국의 대응, 대중에게 노출된 정도, 각국의 경제에 미치는 영향 등 다양한 요인에 따라 감소세를 보였습니다. 예를 들어, 유럽에서 가장 큰 타격을 입은 스페인은 3월 광고 지출이 전월(2020년 2월) 대비 29% 감소했습니다. 반대로 바이러스가 지역사회로 확산되지 않은 호주의 광고 지출은 전월 대비 6% 감소했습니다.

또한 마케터들은 코로나19를 주제로 한 크리에이티브를 제공하여 응원을 표시하고, 도로변 픽업 및 비대면 택배와 같이 소비자에게 도움이 될 수 있는 상품과 서비스를 제공하거나 어떤 형태로든 자선 활동에 참여해야 할 필요성을 느꼈습니다. 많은 브랜드에게 이러한 방식은 브랜드 인지도를 유지하고 소비자와의 연속성을 유지하면서도 위기 자체를 이용하는 것으로 비춰지지 않는 방법이었습니다.

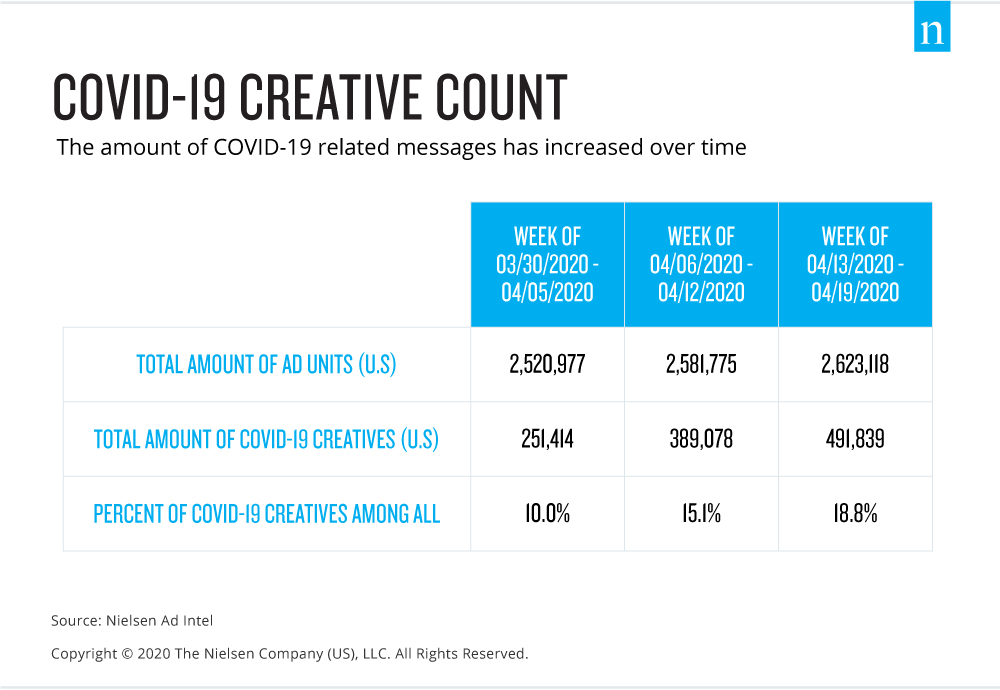

And companies did roll out an increasing amount of ads with COVID-related messages. Nielsen found that from the end of March through the middle of April alone, COVID-themed ads nearly doubled in just a few weeks alone. COVID creative units in the national and local markets jumped from 251,000 units during the week of March 30 to 492,000 units the week of April 13—a 96% increase that signals that brands understood going silent entirely was not an option for long-term health.

Consumers themselves were actually open to trying new brands that they saw as helping people during this time. A survey conducted by Nielsen and Wizer, a consumer insights platform backed by Nielsen, found that 72% of respondents cite a company’s efforts in helping people affected by COVID-19 as a reason they’d consider their brand of consumer packaged goods (CPG). What’s more is that 84% of respondents agreed that companies offering support as consumers comply with COVID restrictions are setting themselves apart from companies that do not.

But with a potential for a second wave of crisis in the fall or winter later this year in the U.S., dependent on states reopening and different emerging scenarios, these COVID-related messages are not simply ways to connect with consumers, but also a core indicator on not just the health of the media market, but also an aggregated look at how that market, and specifically marketers, think of the health of the actual consumers themselves. Declines in COVID-19 themes could act as a barometer for how ready brands think the market is for getting back to focusing on ROI and their traditional core messages. And getting back to business would be that crucial elixir that can help marketers as well as media owners revive any media stagnation.