การเร่งตัวของการเปลี่ยนผ่านสู่ระบบดิจิทัลในอุตสาหกรรมต่างๆ ทั่วโลกในช่วงปีที่ผ่านมาทำให้ธุรกิจต่างๆ สามารถดำเนินการต่อไปได้ในโลกที่ไม่มีการโต้ตอบแบบพบหน้ากัน แม้ว่าการนำธุรกิจเข้าสู่ประสบการณ์เสมือนจริงจะเป็นเรื่องที่น่าประทับใจ แต่การเปลี่ยนผ่านสู่ระบบดิจิทัลเป็นเพียงจุดเริ่มต้นสำหรับแบรนด์ต่างๆ ที่ต้องการสร้างความสัมพันธ์ที่แข็งขันและดีต่อสุขภาพกับผู้บริโภค

This is particularly relevant for financial services companies that have historically maintained relatively passive relationships with consumers. That’s because staying operational doesn’t guarantee brand loyalty, especially as traditional banks continue to cite the need to improve their customer experiences. Awareness is key, as the recent Digital Banking Report acknowledges that consumer trust in traditional banks continues to recede. The pullback in ad spend last year is another factor reducing top-of-mind awareness among consumers.

The call to action for marketers in financial services is no different from other industries: connect with people and build meaningful relationships based on true needs. For some financial services companies, however, that will mean overcoming preconceived notions and offering more than virtual replications of existing experiences.

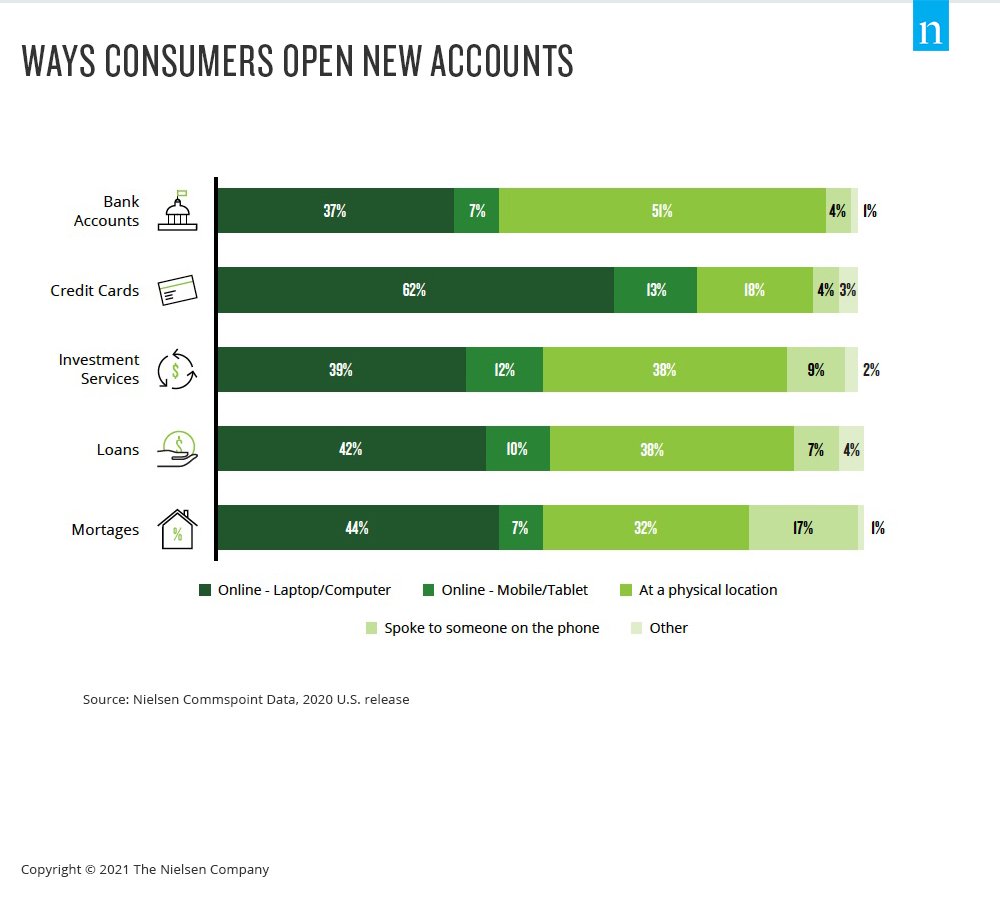

Even before the pandemic, 55% of Americans said they were using digital banking offerings, with an 11% increase in usage over the previous three years among consumers over 40. And Nielsen Commspoint data shows that online channels are becoming the dominant way consumers obtain most financial products, including credit cards and new bank accounts.

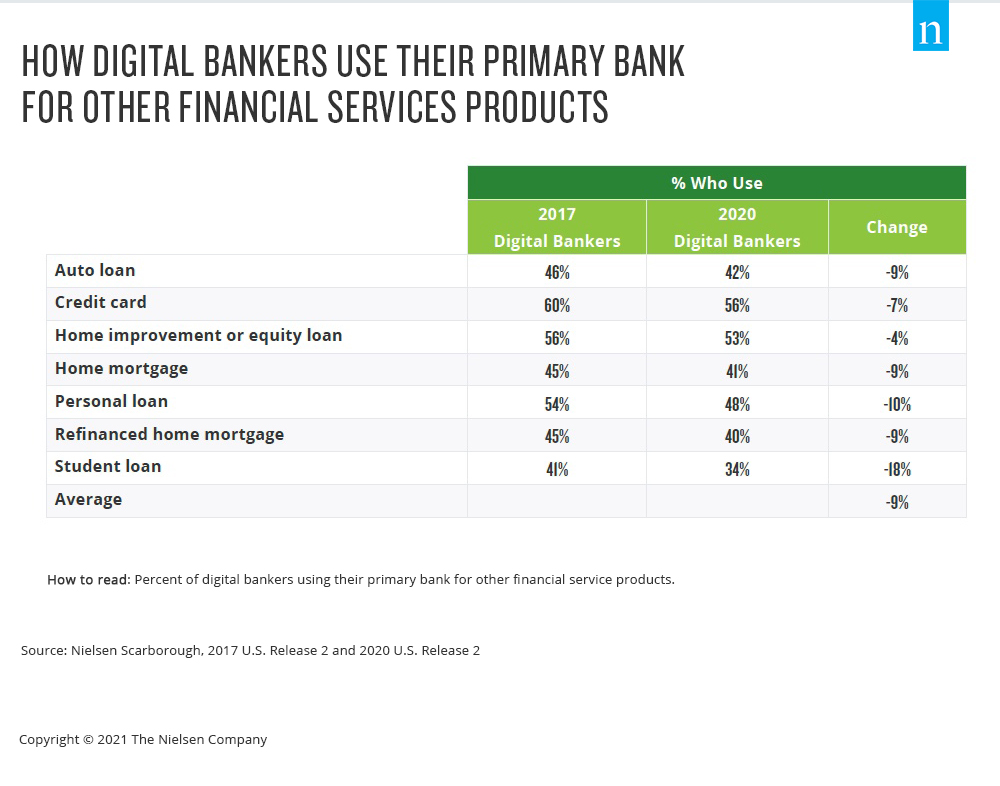

The downside amid the progressively digital landscape is that financial services consumers are increasingly gravitating to new companies—not their primary banks—for their financial services needs. To many people, banks are steadfast financial services institutions, but the relationship between traditional banks and consumers has been fragmenting for years. Fewer than half of U.S. bank customers consider their bank to be their primary financial services provider, according to data from Nielsen Scarborough, and the number is declining. What’s more, consumers are increasingly less inclined to use their primary bank for financial services products like home loans and credit cards.

ประชาธิปไตยที่ขับเคลื่อนด้วยเทคโนโลยีเป็นปัจจัยหนึ่งที่ทำให้ความสัมพันธ์ระหว่างธนาคารกับลูกค้าแตกแยกกัน ในความเป็นจริงแล้ว ธนาคารดิจิทัลมีแนวโน้มที่จะใช้ธนาคารหลักของตนสำหรับความต้องการด้านบริการทางการเงินเสริมน้อยกว่าธนาคารที่ไม่ใช่ดิจิทัลถึง 20% การเพิ่มขึ้นของผู้เล่นที่ไม่ใช่แบบดั้งเดิมในบริการทางการเงินมีผลเช่นเดียวกับผู้มาใหม่ในพื้นที่การสตรีมวิดีโอ นั่นคือ มีตัวเลือกมากขึ้น ผู้บริโภคจึงสามารถสืบค้นและลองใช้งานได้มากขึ้น เมื่อคุณรวมตัวเลือกนี้เข้ากับธรรมชาติของความสัมพันธ์แบบเฉื่อยชาระหว่างองค์กรบริการทางการเงินกับผู้บริโภคมาโดยตลอด ผลิตภัณฑ์หรือบริการใหม่ที่เพิ่งเข้ามาพร้อมความพยายามทางการตลาดแบบมีเสียงพูดมักจะเพียงพอที่จะทำให้ผู้คนคิดที่จะเปลี่ยนแปลง

ซึ่งหมายความว่า ในขณะที่ความต้องการของผู้บริโภคต่อบริการดิจิทัลเติบโตขึ้น ประสบการณ์เสมือนจริงที่สะท้อนถึงประสบการณ์แบบดั้งเดิมนั้นไม่ได้ดึงดูดโอกาสทั้งหมดได้ เมื่อเผชิญกับโลกที่นิสัยและความชอบเปลี่ยนไป นักการตลาดในบริการทางการเงินที่เป็นผู้นำในแนวทางดังกล่าวกำลังดำเนินการดังกล่าวโดยการมีส่วนร่วมกับลูกค้าในรูปแบบที่มีความหมาย โดยมุ่งเน้นไปที่กลยุทธ์การตลาดแบบต่อเนื่องที่สร้างความคุ้นเคยและการเชื่อมโยง

For additional insights, download our Evolving Customer Relationships for Financial Services Marketers report.