昨年、世界の産業界でデジタル化が加速したことで、対面でのやり取りがない世界でもビジネスを継続できるようになった。しかし、ビジネスをバーチャルに体験させることは素晴らしいことだが、デジタル化は、消費者との積極的で健全な関係を育もうとするブランドにとっては、出発点に過ぎない。

This is particularly relevant for financial services companies that have historically maintained relatively passive relationships with consumers. That’s because staying operational doesn’t guarantee brand loyalty, especially as traditional banks continue to cite the need to improve their customer experiences. Awareness is key, as the recent Digital Banking Report acknowledges that consumer trust in traditional banks continues to recede. The pullback in ad spend last year is another factor reducing top-of-mind awareness among consumers.

The call to action for marketers in financial services is no different from other industries: connect with people and build meaningful relationships based on true needs. For some financial services companies, however, that will mean overcoming preconceived notions and offering more than virtual replications of existing experiences.

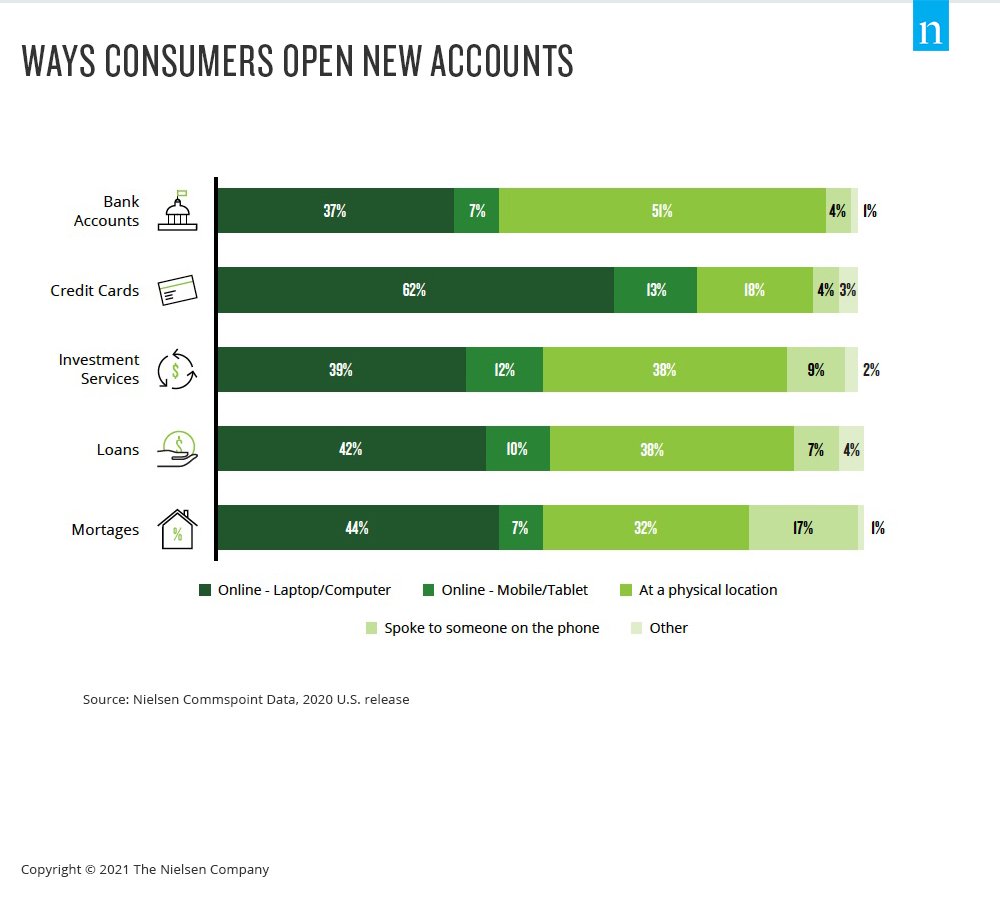

Even before the pandemic, 55% of Americans said they were using digital banking offerings, with an 11% increase in usage over the previous three years among consumers over 40. And Nielsen Commspoint data shows that online channels are becoming the dominant way consumers obtain most financial products, including credit cards and new bank accounts.

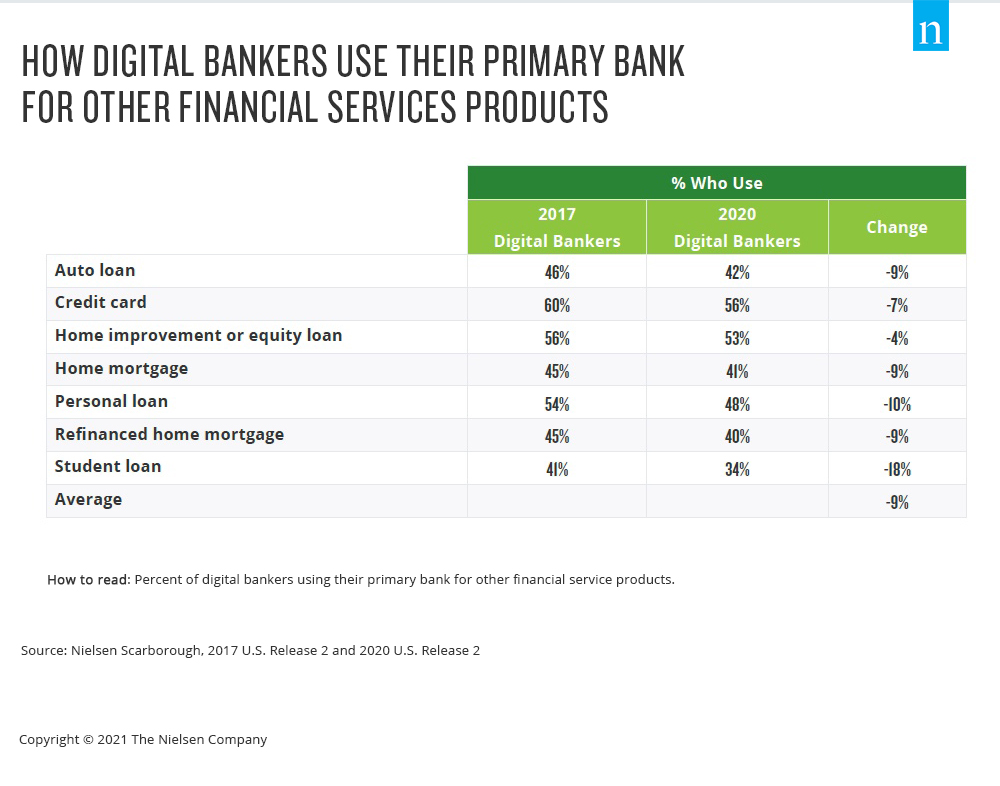

The downside amid the progressively digital landscape is that financial services consumers are increasingly gravitating to new companies—not their primary banks—for their financial services needs. To many people, banks are steadfast financial services institutions, but the relationship between traditional banks and consumers has been fragmenting for years. Fewer than half of U.S. bank customers consider their bank to be their primary financial services provider, according to data from Nielsen Scarborough, and the number is declining. What’s more, consumers are increasingly less inclined to use their primary bank for financial services products like home loans and credit cards.

テック主導の民主化は、銀行と顧客の関係を分断する要因となっている。実際、デジタル・バンカーは非デジタル・バンカーに比べ、付随的な金融サービス・ニーズに主要銀行を利用する割合が20%低い。金融サービスにおける非従来型プレーヤーの増加は、ビデオストリーミング分野への新規参入と同じ効果をもたらす。選択肢が増えるということは、消費者がより多くのことを調べ、試してみることを意味する。この選択肢と、金融サービス機関と消費者との関係が歴史的に受動的なものであったことを組み合わせると、声高なマーケティング活動を伴う新たな商品やサービスの参入が、多くの場合、人々の考え(ニールセンについて )を変えるために必要なすべてとなる。

つまり、デジタル・サービスに対する消費者の需要が高まる一方で、従来型のバーチャル体験では、その機会を十分に捉えることができないということだ。習慣や嗜好が変化した世界に直面し、先頭を走っている金融サービスのマーケターは、有意義な方法で顧客と関わり、親近感とつながりを構築する常時オンのマーケティング戦略に注力している。

For additional insights, download our Evolving Customer Relationships for Financial Services Marketers report.