지난 한 해 동안 전 세계 산업 전반에 걸쳐 디지털화가 가속화되면서 기업은 대면 상호 작용이 없는 세상에서도 비즈니스를 계속 운영할 수 있게 되었습니다. 그러나 비즈니스를 가상 경험으로 구현하는 것은 인상적이지만, 디지털화는 브랜드가 소비자와 적극적이고 건강한 관계를 구축하고자 하는 출발점일 뿐입니다.

This is particularly relevant for financial services companies that have historically maintained relatively passive relationships with consumers. That’s because staying operational doesn’t guarantee brand loyalty, especially as traditional banks continue to cite the need to improve their customer experiences. Awareness is key, as the recent Digital Banking Report acknowledges that consumer trust in traditional banks continues to recede. The pullback in ad spend last year is another factor reducing top-of-mind awareness among consumers.

The call to action for marketers in financial services is no different from other industries: connect with people and build meaningful relationships based on true needs. For some financial services companies, however, that will mean overcoming preconceived notions and offering more than virtual replications of existing experiences.

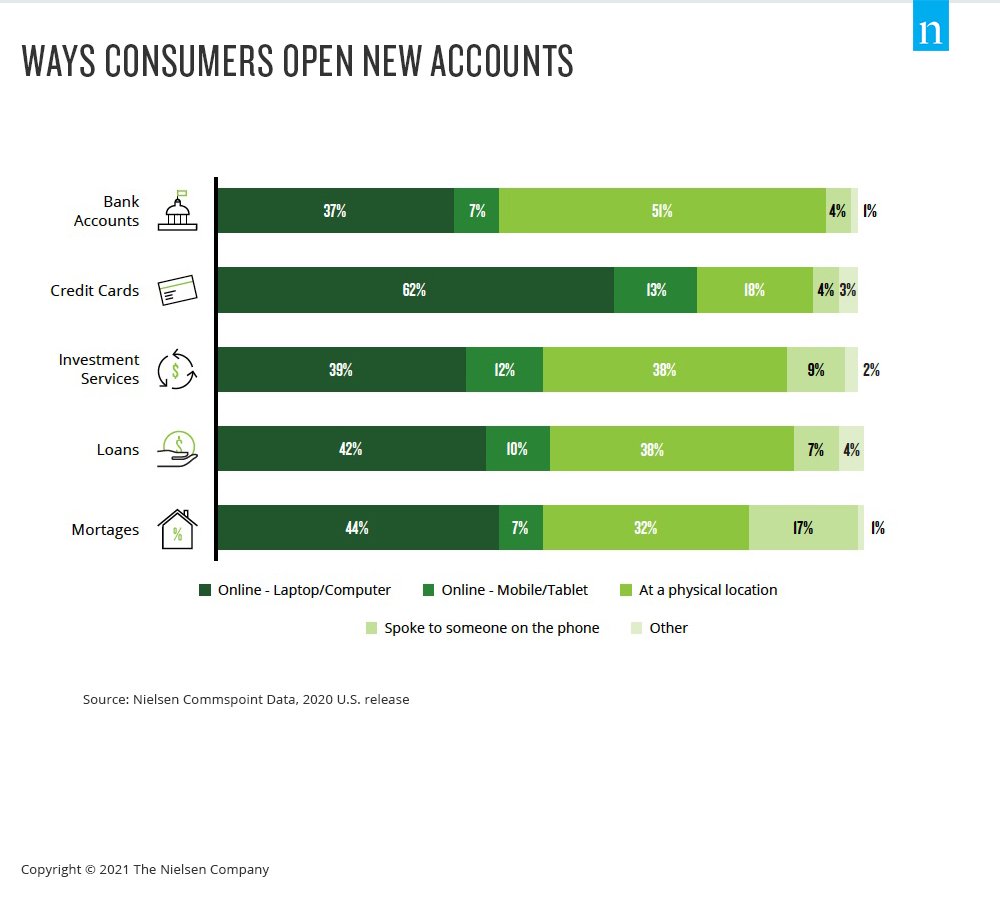

Even before the pandemic, 55% of Americans said they were using digital banking offerings, with an 11% increase in usage over the previous three years among consumers over 40. And Nielsen Commspoint data shows that online channels are becoming the dominant way consumers obtain most financial products, including credit cards and new bank accounts.

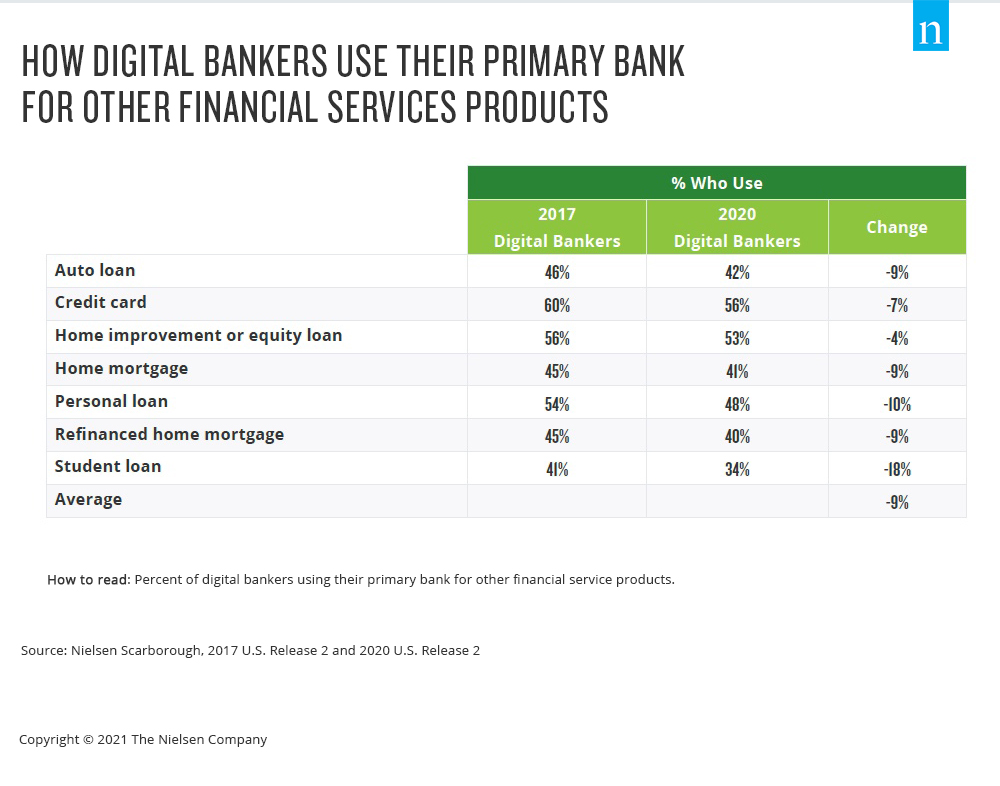

The downside amid the progressively digital landscape is that financial services consumers are increasingly gravitating to new companies—not their primary banks—for their financial services needs. To many people, banks are steadfast financial services institutions, but the relationship between traditional banks and consumers has been fragmenting for years. Fewer than half of U.S. bank customers consider their bank to be their primary financial services provider, according to data from Nielsen Scarborough, and the number is declining. What’s more, consumers are increasingly less inclined to use their primary bank for financial services products like home loans and credit cards.

기술 주도의 민주화는 은행과 고객 간의 관계를 분열시키는 요인이 되었습니다. 실제로 디지털 뱅커는 비디지털 뱅커에 비해 부수적인 금융 서비스 필요 시 주거래 은행을 이용할 확률이 20% 낮습니다. 금융 서비스에서 비전통적인 플레이어의 증가는 비디오 스트리밍 분야의 신규 진입자와 같은 효과를 가져옵니다. 선택의 폭이 넓어진다는 것은 소비자가 조사하고 시도할 수 있는 것이 많아진다는 것을 의미합니다. 이러한 선택권과 역사적으로 수동적이었던 금융 서비스 조직과 소비자 간의 관계 특성을 결합하면, 새로운 상품이나 서비스 진입자가 대대적인 마케팅 활동을 펼치는 것만으로도 사람들이 변화를 고려하게 되는 경우가 많습니다.

즉, 디지털 서비스에 대한 소비자 수요는 증가했지만 기존 서비스를 그대로 답습하는 가상 경험으로는 기회를 충분히 포착하지 못하고 있습니다. 습관과 선호도가 변화하는 세상에 직면하여 이를 선도하는 금융 서비스 마케터들은 의미 있는 방식으로 고객과 소통함으로써 친숙함과 유대감을 형성하는 상시 마케팅 전략에 집중하고 있습니다.

For additional insights, download our Evolving Customer Relationships for Financial Services Marketers report.