Wahrscheinlich war die Welt noch nie so sehr auf Konnektivität angewiesen wie im vergangenen Jahr. Da ein Großteil der Welt immer mehr Zeit zu Hause verbringt, ist die Technologie zur Lebensader für alles geworden, vom Handel über gesellschaftliche Zusammenkünfte bis hin zur neuesten Unterhaltung. Über diese Bereiche ist schon viel geschrieben worden, aber wenn man bedenkt, dass die Konnektivität Millionen von Amerikanern die Möglichkeit gibt, von zu Hause aus zu arbeiten, und zahllosen Kindern im ganzen Land den Zugang zu virtuellem Schulunterricht ermöglicht, kann man mit Fug und Recht behaupten, dass virtuell das neue IRL ist.

That has inspired many Americans to think about where they want to live. Especially if a physical office location is no longer a consideration, the idea of relocation becomes a real option, particularly for those seeking to escape the density of heavily populated urban areas. Many consumers sought temporary solace away from big cities early on, but the prolonged duration of the COVID-19 pandemic has metro-dwellers thinking about more permanent moves, especially as many work-from-home and remote schooling arrangements remain intact.

The prospect of moving could have long-lasting implications for the distribution of the U.S. population. According to recent Oliver Wyman research, one in five urban dwellers is planning to move or considering a move because of the pandemic. And we’re already starting to see the shift. In looking at Nielsen’s year-over-year U.S. household data, we can see increases in an array of smaller-sized designated market areas (DMAs). Many of the increases represent changes of less than 2%, but a handful have been more significant, with the Charlottesville, Va., DMA registering a 16.6% increase in households between the 2019-2020 and 2020-2021 universe estimate periods.

Dieser Trend ist wichtig für Marken und Werbetreibende, die mit den Verbrauchern in Kontakt bleiben wollen, da sich ihre Gewohnheiten - und ihre Lebensräume - ändern.

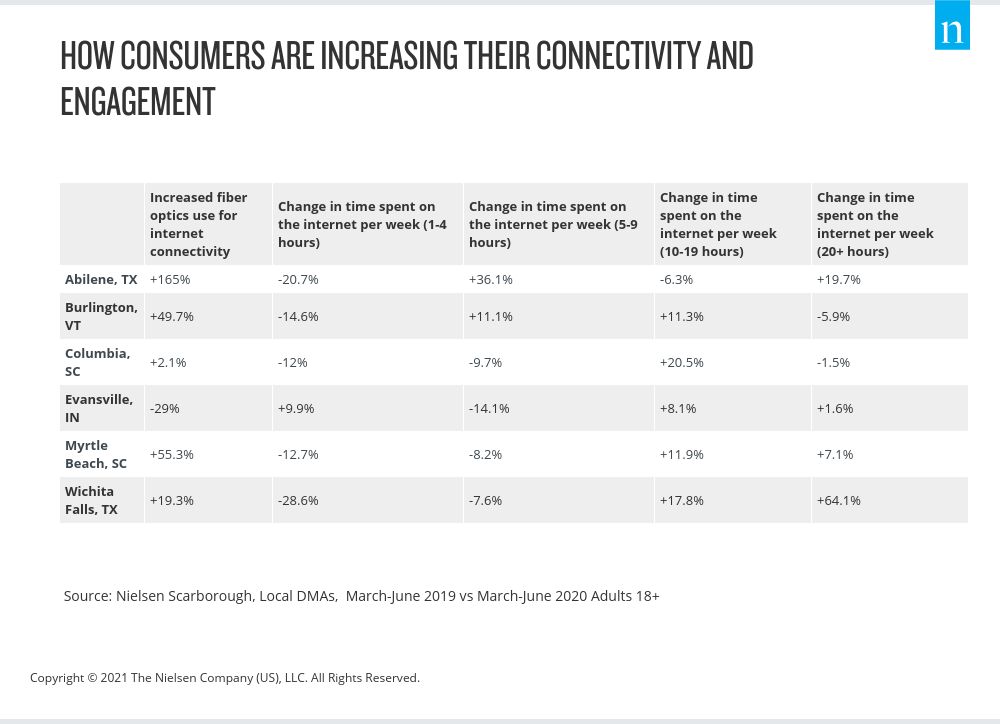

Importantly, many of the country’s lesser-populated DMAs present a valuable opportunity given how digitally engaged their residents are. Whether they’re in cities in Texas, South Carolina, Indiana, Florida or Colorado, consumers in these markets are spending more time connected online. In Abilene, Texas, for example, which is just over 200 miles away from Austin, household use of fiber optics connectivity had increased 165% according to the survey data from Nielsen Scarborough. That connectivity has facilitated a 36% increase in usage of five to nine hours online per week, as well as nearly a 20% increase in usage of 20 hours or more online. In some DMAs, such as Myrtle Beach, S.C., and Wichita Falls, Texas, we’re seeing decreases in internet usage across shorter periods of time and increases in usage across longer periods of time.

Die Verbraucher verbringen nicht nur immer mehr Zeit mit der Nutzung des Internets, sondern folgen auch in vielen weniger bevölkerten Gebieten dem landesweiten Trend, sich in den wachsenden Bereich des Streamings und des Video-on-Demand zu begeben. Im zweiten Quartal 2020 verbrachten die US-Verbraucher durchschnittlich 1 Stunde und 14 Minuten pro Tag mit ihren internetfähigen Geräten, vor einem Jahr waren es nur 50 Minuten. Ein Großteil dieser Zeit wird mit dem Ansehen von Streaming-Inhalten verbracht, die laut Nielsen TV-Messungen im Dezember 2020 23 % der gesamten Fernsehzeit in Haushalten mit Streaming-Fähigkeit ausmachten. Und während die fünf großen Streaming-Video-on-Demand-Plattformen (Netflix, Amazon Prime, Disney+, Hulu und YouTube) 53 % der wöchentlichen Streaming-Minuten auf sich vereinen, entfallen die restlichen 47 % auf die unzähligen Anbieter der Kategorie "Sonstige".

Multichannel video programming distributors (MVPDs; traditional cable companies that augment traditional delivery with a streaming app) and virtual MVPDs are newer to the streaming landscape, but accounted for 36% of the “other” category as of July 2020. They’re also gaining in popularity across many of the country’s lesser-populated DMAs, including Abilene, Burlington and Evansville. In Abilene, for example, Nielsen Scarborough survey data shows that consumers’ past 30-day usage of Sling TV (a subscription-based vMVPD) was almost 235% higher than during the previous survey period. Consumers in the Burlington, Vt.-Plattsburgh, N.Y. DMA report an increase of nearly 102%. Comparatively, consumers in Abilene and Burlington report increased or flat usage of the more traditional SVOD services, but the reported increases were notably lower than those reported for vMVPD usage.

Importantly, despite the growing streaming options available to consumers (including free ad-supported offerings), many are focused on premium offerings. For example, according to Nielsen Scarborough data, consumers in Evansville report more than a 5% decrease in using an internet-connected device or app to watch free TV programs. In Myrtle Beach, consumers report a decrease of 26%. In combination with increased stated usage around paid video options, it’s clear that consumers in these DMAs are gravitating toward what interests them rather than what’s free. This speaks volumes about the value of quality content—even as the market is seeing an array of free, ad-supported options come to market. And when you consider that adults 18 and older were spending an average of almost 11-and-a-half hours with media each day as of June 2020, knowing which platforms and programs they’re engaging with—and the markets where they’re engaging—couldn’t be more important.